About

The Government of India has set targets to achieve 175 GW of installed renewable energy capacity by 2022. To meet this target, around USD 189 billion of investment will be required from 2016 to 2022. It would be extremely difficult to meet this investment requirement through domestic investment only.

The FX Hedging Facility is a customizable currency hedging product that lowers currency hedging costs by slicing the risk of adverse currency fluctuation into different tranches and allocating it to different stakeholders, while maintaining the exposure of the borrower to manageable levels.

Foreign investment is a potential source of significantly more finance for renewable energy in India.However, currency risk is a major deterrent to many foreign investors, resulting in reduced investments in the country due to the higher perception of risk, and necessitating the use of a currency hedge (or foreign exchange swap) to protect against the devaluations, which can add significant costs to transactions.

A simple way to reduce the cost of currency hedging is to provide a direct subsidy to a market swap. However, this may not be an efficient use of the subsidy. Moreover, the subsidy is non-recoverable even if the currency does not depreciate as much as expected.If currency risk is broken down into different tranches, then there may be a stronger argument to subsidize the particular tranche of the FX risk, as the FX Hedging Facility does, rather than partially subsidizing the overall currency risk, as is the case for subsidized cross currency swaps. In a sample transaction, where the user is willing to cover currency depreciation up to 4.5% per year on fixed annual foreign currency payments, the FX Hedging Facility possesses the following benefits compared to a commercial cross currency swap:

- Elimination of counterparty credit risk and liquidity risk: The transaction structure and the upfront availability of the guarantee fee can eliminate the credit risk. Thus, the credit risk premium, which otherwise gets charged in a currency swap, gets eliminated.

- Better targeting of public grants: The FX Hedging Facility is a more efficient use of public grants, or subsidy, as it covers or targets only a certain tranche of the currency risk

- Additional benefits to donors or users: If the currency depreciation is lower than expected, then the upside benefit remains with the FX Hedging Facility, which can be transferred to the donors or user later. This is a more optimal use of donor capital as compared to what would have been required in a commercial currency swap.

The FX Hedging Facility has the potential to reduce the cost of currency hedging by eliminating the credit risk cost, and to mobilize a minimum of ~$9 of foreign investment per dollar of donor grant, with more than 50% probability that donor grant will be fully recovered.

As a result, in our sample transaction, the FX Hedging Facility has a leverage factor of 9 with more than 50% probability that the entire subsidy will be recovered, while the same reduction in cost of currency hedging by directly subsidizing a cross currency swap has a leverage factor of 6 with no option of any recovery of subsidy.

The FX Hedging Facility is at an advanced conceptual phase with a high-level transaction structure and pricing already defined. A commercial bank has shown interest to become the underwriter of the FX Hedging Facility.

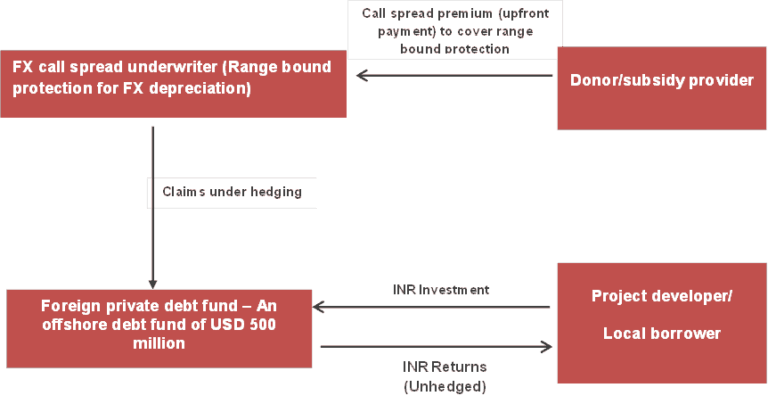

Multiple potential users of the Facility have shown interest in executing pilots of this product. The proponent of the instrument, Mr. Ravindra Rathi of RR Corporate Ltd., has been in advanced discussions with a foreign private debt fund. The fund has shown interest to hedge its current risk using the FX Hedging Facility and subsequently provide the loans to clean energy project developers in India.

The next step would be to seek donor funding for the FX Hedging Facility, which will be used to pay the premiums of FX call spread options upfront.

DESIGN

The FX Hedging Facility can be structured for both debt and equity, depending on the user’s requirements, assuming that these requirements closely follow the structure in the graphic.

Beyond this depreciation rate, and up to a user specified upper limit, the coverage will be provided by the FX risk underwriter.

The upside benefit due to currency depreciation being lower than expected will remain with the hedging facility, and can be returned either to the donor or the user after the tenor of the transaction.

The transaction requires two separate contract agreements by the project developer/investor: one agreement with the hedging facility to cover currency risk up until the customizable annual currency depreciation rate; and another agreement with an FX risk underwriter to cover currency risk beyond that rate till an upper limit, which is P99.7 in our sample transaction.

The equivalent cost of currency depreciation from 0% to the set rate (4.5% in our sample transaction) to be covered by the private debt fund translates into an annualized cost of 528 bps. The cost of the FX risk tranche is underwritten by a commercial entity has been estimated at 134 bps on an annualized basis.