About

Around $40-50 billion of capital investment is required to meet India’s rooftop solar capacity target of 40 GW by 2022, an ambitious leap from current capacity of 1.3 GW. However, currently there are several key barriers which prevent the sector from attracting the required level of investment.

Most individual projects do not have the required scale to raise debt, and are financed solely through equity. This limits the flow of capital to this sector and raises the cost of financing, since equity is usually more expensive than debt. In addition, investors with varying tenor and investment appetites are unable to participate in the rooftop solar sector, due to limited entry/exit options. Finally, limited information on rooftop projects increases return requirements, and pushes up the cost of financing for developers.

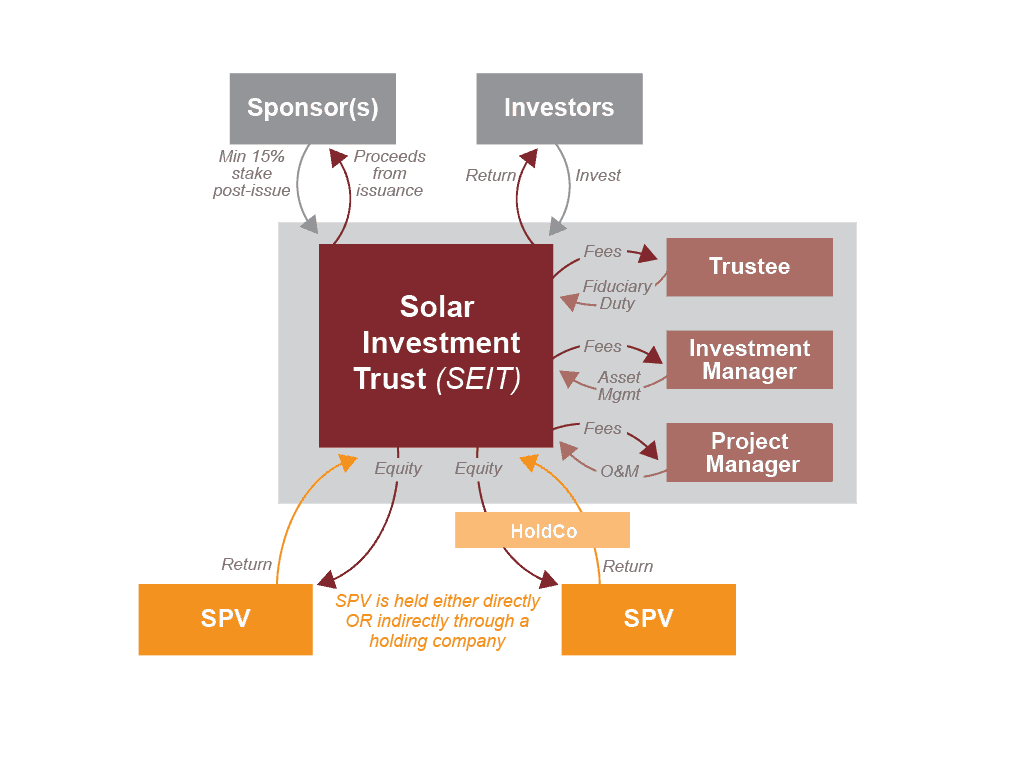

A Solar Investment Trust is an investment vehicle that can help small-scale industrial and commercial rooftop solar developers in India raise equity capital at a lower cost of financing. It is similar to a mutual fund with the primary difference being that the trust can have a direct holding of the project special purpose vehicles (SPVs), while mutual funds usually hold the shares of the company at corporate level and not at the project SPV level.

A Solar Investment Trust is an investment trust for small-scale rooftop solar developers in India, which can raise capital at a lower cost of financing.

An SEIT would be set up as an Infrastructure Investment Trust (InvIT), which is a dividend yielding vehicle in India that is focused on the infrastructure sector. Legally speaking, it is to be set up as a trust, and must abide by the guidelines laid out by Securities and Exchange Board of India (SEBI).

By addressing the investment barriers associated with small-scale projects, Solar Investment Trusts can increase the supply of capital and lower the cost of capital for developers, thereby contributing to the overall growth of the rooftop solar sector.

- Limited Investor Participation: By opening up to new investor classes with different horizons and risk appetites, SEITs will increase the supply of capital. This will lead to greater capital mobilization in the rooftop solar sector.

- Lack of Diversification: By pooling multiple projects, SEITs reduce the non-systematic risk through diversification.

- Lack of Public Information: SEITs will fall within the ambit of SEBI, ensuring corporate governance and disclosure of mandatory information. This will lower the return expectations of investors.

- Illiquidity: Mandatory listing increases liquidity and simplifies the process of entry/exit. This again lowers the cost of capital for the developers.

Based on our estimates, Solar Investment Trusts can potentially mobilize more than USD 1 billion of capital for the rooftop solar sector within the next five years. For the broader clean energy sector, the quantum of capital mobilized by InVITs could easily be in the range of USD 3-4 billion.

Furthermore, Solar Investment Trusts could also easily reduce the cost of equity by 350-400 basis points from the current levels. On the debt side, there will be no significant change in the cost of debt with Solar Investment Trusts. However, we expect SEITs to increase the level of debt within the overall capital pool, thereby lowering the overall cost of capital for developers. Reduction in the cost of financing will lower the levelized cost of energy (LCOE) and improve the adoption of rooftop solar in India.

Instrument Design

A Solar Investment Trust would be set up as an InVIT by a renewable energy developer, who would also appoint the trustee, investment manager, and the project manager. The developer will then transfer shares of special purpose vehicles (SPVs) to the SEIT and give up a percentage of ownership to unit holders, in exchange for capital.

Since the SEIT would be a listed instrument falling under the ambit of SEBI (Securities Exchange Board of India), it will be able to widen the investor base and ensure participation from institutional investors and corporate entities, who might otherwise be hesitant to invest in unlisted rooftop solar projects.

Furthermore, once the SEIT is set up, the developer or the sponsor can continually transfer shares of projects (SPVs) to the trust in exchange for fresh capital. Since an InvIT is an independent entity, all such investments will have to be approved by the trustee and the investment manager so that interests of unitholders are safeguarded.

Thus, SEITs will enable recycling of capital for the rooftop solar sector. This means a greater number of projects can be undertaken using the same amount of capital. For a sector such as the rooftop solar sector, that is short on capital, capital recycling is quintessential.

As highlighted previously, the inherent structure of the SEIT, as an InVIT, (in terms of providing diversification, and mandating listing and information disclosures) allows developers to raise capital at a lower cost. This will lower the long-term levelized cost of electricity and boost rooftop solar adoption in India.